NJ 1065 Instructions: An Excellent Guide

Table of Contents

A Guide To Unlock NJ 1065 Instructions

Form NJ-1065, issued by the New Jersey Division of Taxation, is the partnership return used to report income, gains, losses, deductions, and other financial information from partnerships doing business in New Jersey. This applies to structures like general partnerships, limited partnerships, limited liability partnerships, and LLCs taxed as partnerships.

All partnerships conducting business or deriving income from New Jersey sources must file Form NJ-1065, regardless of whether the entity owes tax.

Today we cover a step by step guide on NJ 1065 instructions.

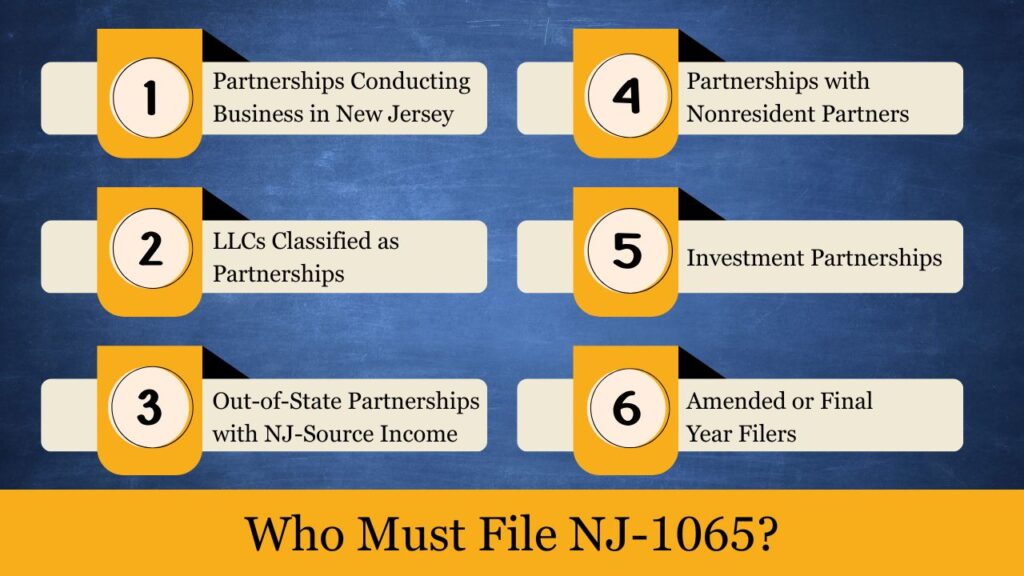

Who Must File NJ-1065?

Engaging in business in New Jersey triggers a Form NJ-1065 filing requirement for any partnership or LLC considered a partnership for federal tax purposes. The requirement applies regardless of whether the entity has any net income or tax liability.

Here’s a detailed breakdown of the entities required to file:

1. Partnerships Conducting Business in New Jersey

Any domestic or foreign partnership—including general partnerships, limited partnerships (LPs), and limited liability partnerships (LLPs)—that carries out business operations, owns property, or maintains a physical or economic presence in New Jersey is required to file Form NJ-1065.

Examples:

- A real estate partnership that owns rental property in New Jersey.

- A consulting firm with an office or employees located in the state.

- A service-based partnership with New Jersey clients or contracts.

2. LLCs Classified as Partnerships

An LLC with two or more members that has elected to be treated as a partnership for federal tax purposes must also file NJ-1065 if it:

- Is formed in New Jersey,

- Holds registration or approval to operate within the state of New Jersey, or

- Derives income from New Jersey sources.

Even if the LLC does not have a physical location in NJ but earns revenue through services, sales, or other operations within the state, it still falls under the filing requirement.

3. Out-of-State Partnerships with NJ-Source Income

Partnerships operating outside New Jersey but earning income from within the state are required to file Form NJ-1065. This includes:

- Rental income from properties located in NJ,

- Sales of tangible goods delivered to customers in NJ,

- Services rendered in New Jersey, or

- Investments that produce income allocated to NJ under NJ allocation rules.

4. Partnerships with Nonresident Partners

If a partnership has one or more nonresident partners (individuals, estates, or corporations) and NJ-source income is allocated to them, the partnership:

- Must file NJ-1065, and

- Required to withhold and remit tax for nonresident partners unless they are covered by a composite return (Form NJ-1080-C) or qualify for an exemption under an applicable tax treaty.

5. Investment Partnerships

Investment partnerships are generally required to file NJ-1065 if:

- They derive NJ-source income, or

- Their total gross income exceeds $6,000.

However, small investment clubs may qualify for exemption if they meet specific criteria:

- 20 or fewer members,

- Passive investment income only,

- No active management or services rendered,

- Each member manages their own tax reporting.

6. Amended or Final Year Filers

- Partnerships that need to correct a previously filed NJ-1065 must file an amended return.

- Partnerships that are closing or liquidating operations in New Jersey must file a final NJ-1065 return and indicate it accordingly.

Entities Not Required to File NJ-1065

- Single-member LLCs treated as disregarded entities for federal tax purposes.

- Entities classified as C corporations or S corporations should file Form CBT-100 or CBT-100S, respectively, instead of the partnership return.

- Partnerships that are not conducting business and have no New Jersey-sourced income or presence.

Filing Deadline for NJ-1065

Partnerships that are required to file New Jersey Form NJ-1065 must adhere to specific deadlines set by the New Jersey Division of Taxation. Filing on time is critical to avoid penalties, interest, or issues with partner-level tax credits or composite filings.

Standard Filing Deadline

For partnerships operating on a calendar year basis, the filing deadline for NJ-1065 is April 15, 2025.

If the partnership operates on a fiscal year, the deadline is the 15th day of the fourth month following the close of the partnership’s fiscal year.

Examples:

- Partnerships operating on a calendar year ending December 31, 2024, are required to file their return by April 15, 2025.

- A partnership with a fiscal year ending June 30, 2024, must file by October 15, 2024.

Extension of Time to File

If additional time is needed to prepare and file the return, partnerships may request an extension by filing Form PART-200-T.

Key Points about Extensions:

- The extension grants an additional 5½ months to file the return.

- For calendar year partnerships, the extended due date would be September 30, 2025.

- The extension only applies to the time to file—not to the time to pay any taxes due.

- Any entity-level fee or nonresident partner tax must still be paid by the original due date (April 15 for calendar year filers).

To receive the extension, the form must be filed on or before the original NJ-1065 due date.

Payment Obligations by Deadline

Even if the return is extended, partnerships must still ensure the following are paid by the regular due date to avoid penalties and interest:

- Entity-level filing fees (if applicable),

- Nonresident partner tax payments, and

- Any applicable composite tax payments for nonresident individuals.

These payments can be made electronically through the New Jersey Division of Taxation’s online payment system or by mail using a voucher.

Late Filing Consequences

Failing to file NJ-1065 by the due date (without an approved extension) may result in:

- Late filing penalties ($100 per month, up to a maximum of $500),

- Interest on unpaid taxes, and

- Invalidation of tax credits or overpayment claims at the partner level.

Timely filing also ensures partners receive their Schedule NJK-1s promptly, enabling them to report their share of income or loss on their individual or business returns without delay.

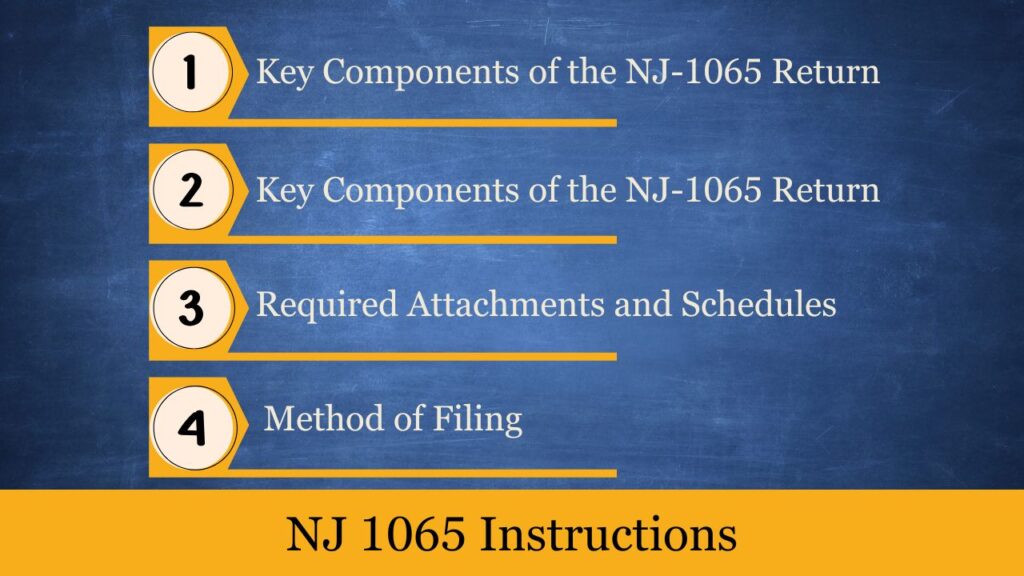

NJ 1065 Instructions

Filing Form NJ-1065 involves not only submitting the return itself, but also accurately reporting partnership-level and partner-level income, complying with New Jersey allocation rules, and fulfilling tax obligations for nonresident partners. The return must be complete, include all required schedules and attachments, and follow New Jersey-specific reporting standards, which may differ from the federal Form 1065.

1. Basic Filing Requirement

All partnerships (including LLCs classified as partnerships for federal purposes) must file NJ-1065 if they:

- Conduct any business activity in New Jersey,

- Derive income from New Jersey sources,

- Have New Jersey resident partners, or

- Have nonresident partners allocated income from NJ sources.

This applies whether or not the entity owes tax or has net income. Even partnerships with no income but active registration in NJ are often still required to file.

2. Key Components of the NJ-1065 Return

Filing Form NJ-1065 (Partnership Return) involves more than just reporting total income or filing a checklist. It requires a detailed breakdown of partnership-level activity and the individual income allocations made to each partner, strictly in accordance with New Jersey tax laws. The form includes several sections and schedules that must be completed thoroughly and accurately.

Below are the core components of the NJ-1065 return, along with what each section entails:

a. Partnership Information Section

This is the opening section of the return and includes general identifying details such as:

- Partnership Name & Address

- Federal Employer Identification Number (FEIN)

- Business Activity Code (6-digit NAICS code describing the primary business)

- Date of Formation

- NJ Corporation/Entity ID (if registered with the state)

- Tax Year Information (calendar or fiscal)

- Indicators such as:

- Specify whether the return is an initial filing, a final return, or an amended submission

- Indicate whether the partnership is opting to submit a composite return on behalf of its nonresident partners

- Does it have any nonresident partners?

This section establishes the identity and filing context of the partnership.

b. Summary of NJ-Source Income and Deductions

This is one of the most important parts of the return. It requires the partnership to report only New Jersey-sourced income and allowable deductions, even if federal amounts are higher or different.

Items reported here include:

- Ordinary business income or loss

- Guaranteed payments to partners

- Rental income or loss

- Dividends, interest, royalties

- Net capital gain or loss

- Other income (e.g., cancellation of debt, Section 1231 gains)

Deductions may include:

- Salaries and wages (if NJ-based)

- Rent or lease payments for NJ property

- NJ-eligible depreciation and amortization

- Contributions, if made to NJ-recognized charities

Each line in this section should reflect income earned or expenses incurred within New Jersey, as the state does not tax income sourced outside its jurisdiction.

c. Schedule A – Partner Information Summary

Schedule A is a required component listing detailed information about every partner, including:

- Full Name and Mailing Address

- Provide a Social Security Number for individuals or an Employer Identification Number for business entities

- Ownership percentage at beginning and end of the tax year

- Classification (e.g., individual, corporation, trust, partnership)

- Residency status (New Jersey resident vs. nonresident)

- Status as a general or limited partner

This schedule helps the Division of Taxation track ownership changes, partner allocations, and applicable filing requirements for each participant.

d. Schedule NJK-1 – Partner’s Share of Income

The Schedule NJK-1 must be prepared for each partner and provided to them after the partnership return is filed. It shows:

- The partner’s share of New Jersey-source income

- Allocations of different income types (e.g., ordinary business income, interest, rental income)

- Adjustments specific to New Jersey (e.g., bonus depreciation, tax-exempt interest)

- Amount of tax paid or withheld on behalf of the partner

- Include applicable credits, such as those for taxes paid to other states or jurisdictions

This form is essential for each partner to accurately complete their own NJ-1040, NJ-CBT, or composite return if applicable.

e. Schedule B and NJ-NR-A/NJ-NR-B – Nonresident Partner Tax Computation

If any partners are nonresidents of New Jersey, the partnership is obligated to:

- Compute their share of NJ-source income

- Withhold tax and remit it to the state unless they participate in a composite return

- Report this using Schedule NJ-NR-A (allocating income) and Schedule NJ-NR-B (tax calculation)

The partnership must either:

- Remit tax at applicable NJ personal income tax rates based on income brackets, or

- File Form NJ-1080-C on behalf of all eligible nonresident individual partners using the flat 6.37% composite rate

f. Form NJ-1065E – Entity-Level Filing Fee Calculation

Partnerships with more than two partners are required to pay a $150 fee per partner, up to a maximum of $250,000 per return. This fee applies regardless of whether the partnership has income or tax liability.

Form NJ-1065E, included in the return package, must be completed to determine the total fee owed. This fee is not deductible on the NJ-1065 return and must be paid by the original filing due date.

g. Attachments and Supporting Documents

A complete NJ-1065 filing includes several supporting attachments:

- A full copy of the federal Form 1065, including all federal Schedule K-1s

- All NJK-1s issued to partners

- Submit apportionment schedules if the partnership operates in more than one state to allocate income appropriately

- Schedule B, Schedule A, NJ-NR-A/B (if applicable)

- Form PART-200-T, if an extension was filed

- Vouchers for any tax payments (e.g., NJ-1065-V)

h. Electronic Filing and Signature

- Most partnerships are required to file NJ-1065 electronically using the New Jersey Division of Taxation’s e-File system or an approved third-party software provider.

- Paper filing is allowed only in limited cases (e.g., specific investment partnerships).

- The return must be signed by a general partner or authorized member, certifying that the information is true and correct to the best of their knowledge.

3. Required Attachments and Schedules

Along with the NJ-1065 form itself, the partnership must also attach:

- Federal Form 1065 (complete copy)

- All federal Schedules K-1

- All Schedules NJK-1 (one per partner)

- Apportionment schedules, if doing business inside and outside NJ

- Extension form (PART-200-T), if applicable

- Payment vouchers for tax or fees remitted

4. Method of Filing

- Electronic Filing is mandatory for most partnerships through New Jersey’s Business Online Filing system or approved third-party e-file providers.

- Paper filing is generally only permitted for partnerships that meet specific exceptions (e.g., certain small investment clubs or entities with no NJ activity).

NJ-1065 Calculation Guide

1. Calculate NJ-Source Income

The core purpose of Form NJ-1065 is to report New Jersey-sourced income earned by the partnership, not the total federal income. Begin with the federal figures (from IRS Form 1065) and adjust them based on New Jersey’s sourcing rules.

A. Start with Federal Ordinary Business Income

From IRS Form 1065:

- Line 22 of federal Schedule K: Ordinary business income (before partner allocations).

B. Adjust for NJ Apportionment or Allocation

If the partnership operates in multiple states:

- Use Schedule J (NJ-1065) to apportion income to NJ using the 3-factor formula:

- Property Factor

- Payroll Factor

- Sales Factor

- Calculate the average and apply it to federal income to determine NJ-source portion.

C. Add/Remove NJ-Specific Adjustments

Adjust for items treated differently under NJ law:

- Add back federally deducted expenses not allowed in NJ (e.g., bonus depreciation).

- Subtract income excluded from NJ taxation (e.g., certain exempt interest).

Result: Total NJ-Source Partnership Income

2. Allocate Income to Partners

Once NJ-source income is determined, divide it among partners based on their ownership percentages or special allocations stated in the partnership agreement.

Each partner’s share is reported on:

- Schedule A (Partner summary),

- Schedule NJK-1 (Partner-specific allocation).

Make sure to identify:

- Resident vs. Nonresident partners (important for withholding),

- Individual vs. corporate partners (affects tax obligations).

3. Calculate Nonresident Partner Withholding Tax

If the partnership has nonresident partners (individuals, trusts, or corporations), it must withhold NJ Gross Income Tax on each partner’s share of NJ-source income, unless:

- The partner joins a composite return, or

- The partner provides a Form NJ-1080-C Waiver (rare).

Steps:

- For each nonresident:

- Multiply their NJ-source income share by the applicable NJ rate.

- Use the top NJ tax rate of 10.75% if the income exceeds $5 million.

- Otherwise, use progressive individual rates.

Alternatively:

- Use flat 6.37% for composite returns (Form NJ-1080-C) filed on behalf of multiple nonresident individuals.

Report this tax on:

- Schedule NJ-NR-A and NJ-NR-B

- Make payment using Form NJ-1065-V

4. Calculate the Entity-Level Filing Fee

If the partnership has more than two owners, it must pay a filing fee based on the number of owners:

| Number of Owners | Filing Fee |

| 3 or more | $150 per owner |

| Maximum Fee | $250,000 total |

Example:

- A partnership with 10 partners:

$150 × 10 = $1,500 filing fee - A partnership with 2 or fewer partners:

No fee due

Report this on:

- Form NJ-1065E (included with NJ-1065)

- Pay with NJ-1065-V or online via NJ e-file system

5. Composite Tax (If Applicable)

If electing to file Form NJ-1080-C for nonresident individual partners:

- Compute the total composite income (combined NJ-source income of all electing nonresidents)

- Multiply by the flat 6.37% rate

- Include this tax payment with NJ-1065 or use NJ-1080-C Payment Voucher

6. Determine Total Amount Due

Total Tax Due = Nonresident withholding tax

- Composite tax (if any)

- Entity-level filing fee – Any overpayments or credits carried forward = Balance due. with NJ-1065

7. Make Payments

Use one or more of the following:

- Form NJ-1065-V for payments made with the return

- Online payments via NJ Division of Taxation’s e-File Services

- Separate vouchers for composite or fee payments

Example Calculation Summary

A partnership has:

- $200,000 in NJ-source income

- 4 equal partners (2 NJ residents, 2 nonresidents)

- Files composite return for both nonresidents

Step 1: Each partner’s income = $50,000

Step 2: Composite tax = $100,000 (2 nonresidents) × 6.37% = $6,370

Step 3: Filing fee = 4 partners × $150 = $600

Step 4: Total amount due = $6,370 + $600 = $6,970

Schedule NJK-1 (Partner’s Share of Income) – Complete Guide

Schedule NJK-1 is a vital part of the New Jersey Form NJ-1065 (Partnership Return). It serves as the state-level equivalent of the federal Schedule K-1 and reports each partner’s share of New Jersey-sourced income, deductions, adjustments, and tax payments. The partnership is required to complete a separate NJK-1 for every partner, resident or nonresident, and provide each partner with a copy to help them prepare their individual or corporate New Jersey tax returns.

Purpose of NJK-1

Schedule NJK-1 ensures proper transparency and tax compliance by:

- Allocating New Jersey-source income and deductions to each partner

- Reporting any New Jersey withholding or composite tax paid on the partner’s behalf

- Disclosing resident status, entity type, and ownership percentage

- Providing the basis for NJ individual, corporate, or fiduciary tax returns

It is used by the New Jersey Division of Taxation to verify the accuracy of tax returns filed by partners and ensure that nonresident withholding rules have been followed.

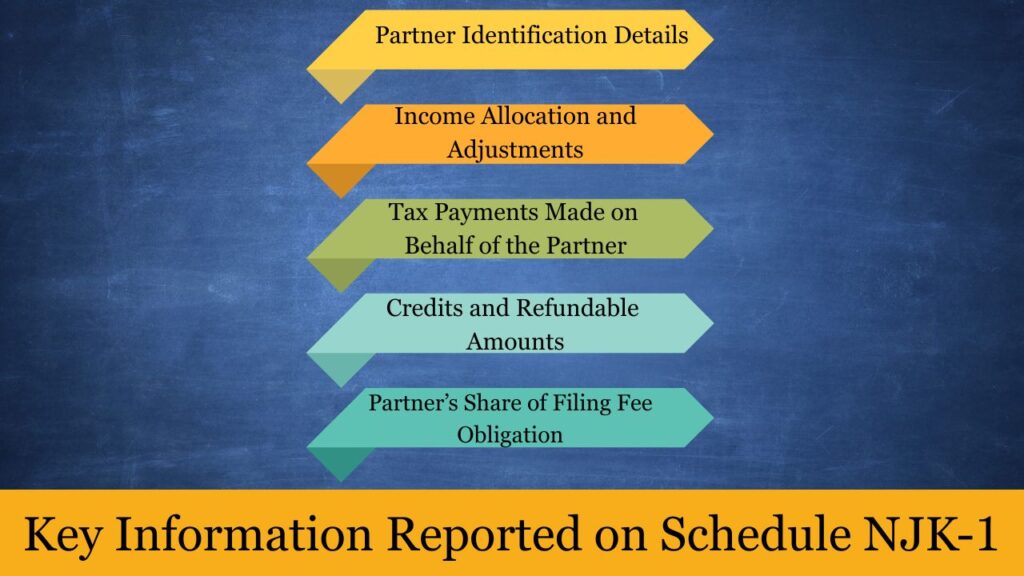

Key Information Reported on Schedule NJK-1

Each Schedule NJK-1 includes detailed data about both the partner and their distributive share of the partnership’s New Jersey-source income.

1. Partner Identification Details

- Partner’s name and mailing address

- Provide the SSN for individuals or the EIN for business entities as applicable

- Type of partner: Individual, C corporation, S corporation, trust, estate, or other

- Resident status: NJ resident or nonresident

- Percentage of ownership, both at beginning and end of the year

2. Income Allocation and Adjustments

- Ordinary business income or loss from NJ sources

- Guaranteed payments received by the partner (if applicable)

- Net rental income, interest, dividends, royalties, or capital gains from NJ activities

- NJ-specific modifications (e.g., bonus depreciation adjustments, tax-exempt interest exclusions)

This section only includes income allocated to New Jersey, in contrast to federal K-1s that report total income regardless of source.

3. Tax Payments Made on Behalf of the Partner

- Withholding tax paid for nonresident partners (based on their NJ-source income)

- Composite tax payments made via Form NJ-1080-C

- These payments are credited on the partner’s individual/corporate NJ return

4. Credits and Refundable Amounts

- Taxes paid to other jurisdictions that may be eligible for credit

- Refundable amounts passed through to the partner, if applicable

5. Partner’s Share of Filing Fee Obligation

Although the entity-level fee is paid by the partnership, the NJK-1 may reflect how the fee was apportioned among partners, especially if required for transparency in internal accounting or tax planning.

How NJK-1 Differs from Federal Schedule K-1

| Feature | Federal K-1 | NJK-1 |

| Income Scope | All income (worldwide) | Only NJ-source income |

| Tax Withholding | Rarely applicable | Nonresident withholding required |

| Filing Requirement | Federal return | Must be submitted with NJ-1065 |

| Purpose | Federal tax reporting | NJ-specific tax compliance |

Filing and Distribution Requirements

- An individual NJK-1 form must be prepared for each partner in the partnership.

- All NJK-1s must be included with Form NJ-1065 when submitted to the state

- Partnerships are required to distribute copies of each NJK-1 to partners by the due date of the return (including extensions)

Extension Requests for NJ-1065 – Form PART-200-T

If your partnership is unable to file Form NJ-1065 (Partnership Return) by the original due date, you may request additional time by submitting Form PART-200-T, the official New Jersey Application for Extension of Time to File Partnership Return.

This form grants eligible partnerships an extension to file their return, but it does not extend the time to make any required payment. Any taxes due, including entity-level fees or nonresident withholding, must still be paid by the original filing deadline to avoid penalties and interest.

Key Highlights of Form PART-200-T

- Purpose: To request an additional 5½ months to file Form NJ-1065.

- Not an extension to pay – all taxes and fees still due by the regular deadline.

- No signature or explanation required—just basic partnership details and estimated payments.

When to File Form PART-200-T

- For calendar-year partnerships, the original due date of NJ-1065 is April 15.

- Therefore, Form PART-200-T must be filed by April 15.

- For fiscal-year partnerships, the due date is the 15th day of the 4th month after the end of the tax year.

If approved, the extension permits an additional 5 months and 15 days beyond the original due date for filing:

- Example: For tax year ending December 31, 2024, the extended deadline becomes September 30, 2025.

Eligibility Criteria for Using PART-200-T

You may file Form PART-200-T if:

- You need extra time to prepare NJ-1065,

- You have made (or will make) all required tax payments by the original due date,

- You are not filing under an automatic federal extension (NJ does not automatically accept IRS Form 7004 for partnerships).

Note: New Jersey does not grant automatic extensions based solely on the federal extension. Form PART-200-T must be filed directly with the state tax authority.

How to File Form PART-200-T

You can file PART-200-T:

Electronically (Preferred Method):

- Through the New Jersey Division of Taxation’s electronic filing system

→ https://www.state.nj.us/treasury/taxation/

By Mail (if electronic filing is not available):

Mail to:

NJDivisionofTaxation

RevenueProcessingCenter

PartnershipExtensionRequest

POBox642

Trenton,NJ08646-0642

What Must Be Paid with the Extension Request

Although filing PART-200-T extends the deadline to file, it does not extend the deadline to pay. The following must still be paid by the original due date (e.g., April 15, 2025):

- Entity-level filing fee (Form NJ-1065E)

- Nonresident partner withholding

- Composite return tax payment (if filing Form NJ-1080-C)

Payments can be made:

- Online via NJ’s e-File system, or

- By mailing payment vouchers (e.g., NJ-1065-V or NJ-1080C-V)

What Happens After Filing PART-200-T

- You do not receive formal approval from NJ. The extension is automatically accepted if filed timely and all estimated taxes are paid.

- If the return is submitted by the extended deadline, it will be treated as filed on time.

- Failure to file the extension form or pay due taxes may result in penalties, including:

- Late filing penalties ($100 per month),

- Interest on unpaid balances,

- Loss of credits or carryforwards.

What to Include with Your NJ-1065 (When Filed Later)

When you eventually file the full NJ-1065 return:

- Be sure to note on the return that it was filed under an approved extension.

- Attach a copy of Form PART-200-T (if mailed), especially if mailing the return.

Conclusion

Filing Form NJ-1065 is a critical annual responsibility for partnerships doing business in or deriving income from New Jersey. Whether your entity has resident or nonresident partners, operates in multiple states, or is subject to New Jersey’s entity-level filing fee, understanding the form’s structure, calculations, and deadlines is essential to maintain compliance.

Frequently Asked Questions (FAQs)

Is NJ-1065 required if my partnership has no income?

Yes, if your partnership is registered or conducting business in NJ, you must file—even if there is no income or activity.

Are single-member LLCs required to file NJ-1065?

No, single-member LLCs are disregarded entities and file as part of the owner’s individual or corporate return.

What if my partnership only holds investments?

Investment partnerships may be exempt from the filing fee but must still file NJ-1065 if they earn NJ-sourced income.